Table of Content

Borrowers of FHA loans must pay mortgage insurance upfront and every month. If you don’t qualify for a conventional mortgage, a mortgage backed by the Federal Housing Administration could be your next best option. These FHA loans have lower income and credit requirements for borrowers. Read on to learn more about FHA loan requirements, how to qualify and apply, get answers to frequently asked questions, and discover if FHA loans are worth it.

The FHA operates solely from its own generated revenue, not any federal taxes. To be able to insure lenders, the agency mandates that borrowers pay FHA funding fees, in the form of mortgage insurance premiums. The FHA, or Federal Housing Administration, provides mortgage insurance on loans made by FHA-approved lenders. FHA insures these loans on single family and multi-family homes in the United States and its territories.

What’s the difference between an FHA inspection and an appraisal?

For Chapter 7 bankruptcy, at least two years must have elapsed and the borrower has either re-established good credit or chosen not to incur new credit obligations. If you don't have an established credit history or don't use traditional credit, your lender must obtain a non-traditional merged credit report or develop a credit history from other means. FHA.com is a privately owned website, is not a government agency, and does not make loans. There are options for homebuyers who have fallen in love with a property that has one of these potentially deal-killing problems. If the inspection reveals the need for roof repairs, and the roof already has three or more layers of roofing, the FHA requires a new roof. The Ascent is a Motley Fool service that rates and reviews essential products for your everyday money matters.

Disclosure of personal property value including any current real estate. The property you want to buy should be your primary house. The Great Depression changed how the United States operated. Many commissions were created to recover the American dream. The Federal Housing Administration was one of those commissions.

Down Payment

Standard FHA guidelines allow for 43% but will sometimes permit a higher DTI, depending on several factors we'll cover next. This type of loan is also a good idea for homebuyers with less-than-perfect credit because FHA loans have lenient credit score requirements. It’s possible to get an FHA loan with a credit score as low as 500. The FHA funding fee includes both the upfront fee and monthly premium that borrowers must pay for mortgage insurance.

The main thing to know about the difference between an FHA inspection and an FHA appraisal is that the FHA does not require an inspection, nor do they have designated inspectors. Simply put, there is no such thing as an FHA inspection. A FICO score of 580 or higher with a lower down payment. Soundness– The structural and foundation conditions must be in satisfactory condition. This means that there can not be any structural damages of any kind which would require repair. The SF Handbook's organizational structure has five main categories that follow the logical flow of a mortgagee or lender's process.

FHA Income Requirements

If your down payment is 10% or more, you'll have to make these payments for 11 years. Many people who can afford the monthly mortgage payments and have reasonable credit will qualify. FHA insured loans require mortgage insurance to protect lenders against losses that result from defaults on home mortgages. Depending on the terms and conditions of your home loan, most FHA loans today will require MIP for either 11 years or the lifetime of the mortgage. Federal Housing Administration loans have requirements, including minimum property standards, which help protect lenders and buyers. To qualify for an FHA loan, borrowers need to have a FICO credit score of at least 500.

An FHA appraiser looks for any damage, hazards, and maintenance issues. Have verifiable employment history for the last two years. A lender should be able to verify your income through pay stubs, tax returns, and bank statements. Tasked with ensuring the working and middle class could secure a home loan, the FHA functions as an alternative to conventional home loans.

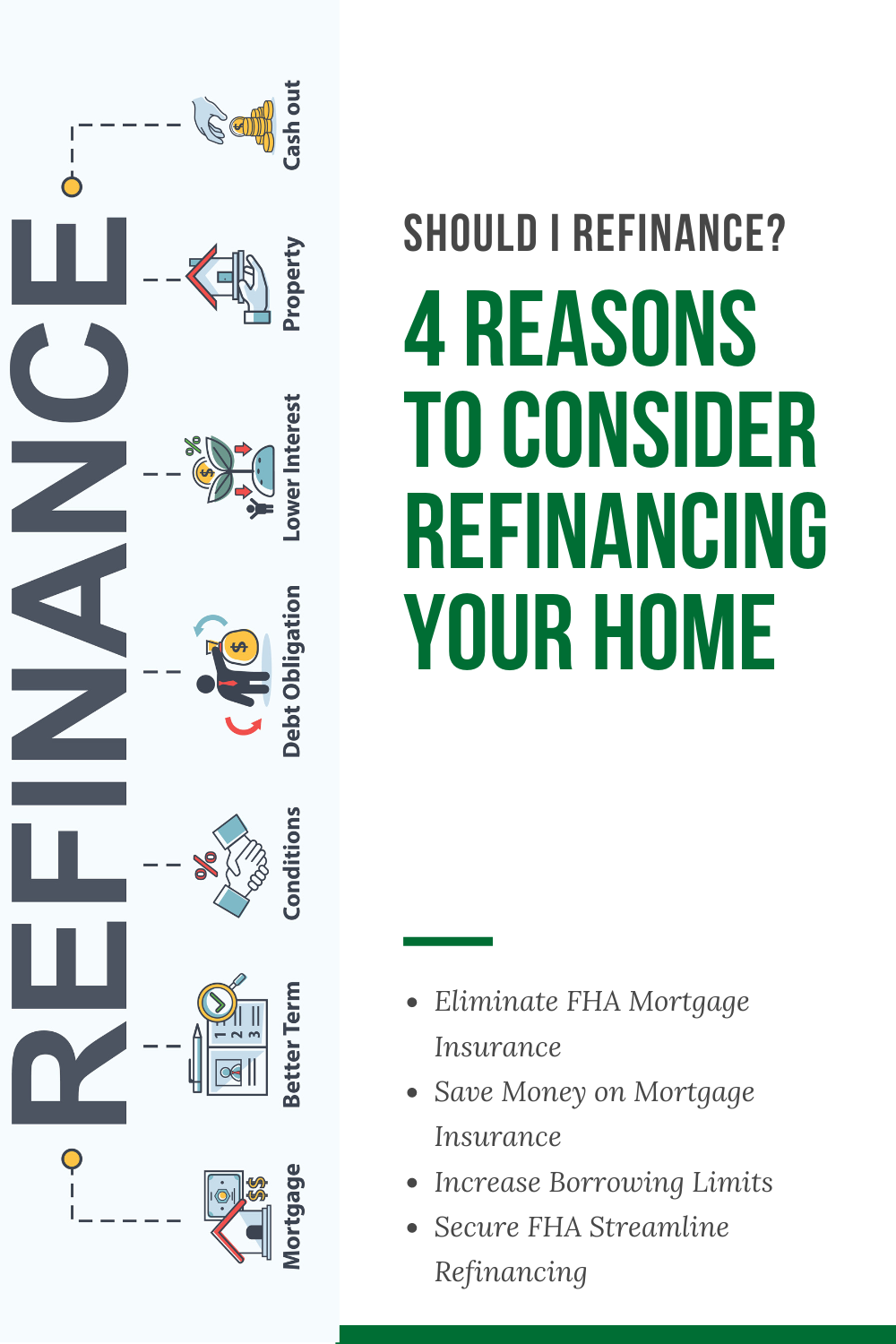

Cash-Out Refinance

Mortgage Insurance premium depends on the size of the down payment. Whereas a lower or 3.5% down payment, you may have to pay MIP for the whole of your life. One of the major factors is house market prices that keeps on fluctuating every year. You can also visit the official website of HUD to know the FHA mortgage limits in a specific country and state.

HUD usually announces loan limit changes in December, for the year following. At a minimum, lenders tend to request pay stubs, W-2 forms, and bank statements. They may also obtain the borrower’s tax returns directly from the IRS. On October 26, the Federal Housing Administration sent out an email to announce some updates to the Single Family Housing Policy Handbook.

The most recognized 3.5% down payment mortgage in the country. A home inspection is an examination of the condition and safety of a real estate property. Alternatively, buyers who can't qualify for an FHA loan may use another loan product, such as an FHA 203 loan, which allows the purchase of a home that has significant problems. In addition to Investopedia, she has written for Forbes Advisor, The Motley Fool, Credible, and Insider and is the managing editor of an economics journal. She is a graduate of Washington University in St. Louis. Many or all of the products here are from our partners that pay us a commission.

Refinance a mortgage, can use an FHA loan as long as they meet the eligibility requirements. In addition to borrower qualifications, the property must meet certain requirements before you can qualify for an FHA mortgage. If you are using a state or local assistance program to obtain an FHA loan, that program may have its own income limits and requirements.

The list is a great starting point if you're not sure where to look. When ready to apply, borrowers need to connect with a third-party lender that offers FHA loan options. Most conventional lenders want a score of 620 or higher, especially in recent years. Some lenders will go down to 580, but most look for buyers with a score of at least 620. Below is a list of the most frequently asked FHA-backed mortgage questions borrowers ask. If you don't see the answer to your question, please reach outto an LGI Homes real estate professional for further assistance.

The process is fairly similar to applying for a non-FHA loan, and depending on the lender, you can kick it off by exploring a mortgage preapproval online or by talking with a loan officer. Browse through our frequent homebuyer questions to learn the ins and outs of this government backed loan program. The first step should be to ask the seller to make the needed repairs. If the seller can't afford to make any repairs, perhaps the purchase price can be increased so that the sellers will get their money back at closing. Usually, the situation works the other way around—if a property has significant problems, the buyer will request a lower price to compensate. However, if the property is already priced below the market or if the buyer wants it badly enough, raising the price to ensure the repairs are completed could be an option.

Appraisal

A home appraiser evaluates the home’s value based on its condition. They will also look at comparable properties to determine how they stack up against similar ones. An FHA appraiser looks at the interior and exterior of the property to ensure it meets the FHA’s Minimum Property Standards. They take photos and make notes based on their observations and any problems.

It is the largest insurer of residential mortgages in the world, insuring tens of millions of properties since 1934 when it was created. This means that you could, for example, find an FHA lender with a credit score requirement well into the 600s. You would need to meet this requirement in order to take out an FHA loan through that lender. FHA loan requirements are relatively straightforward, but lenders can impose their own minimums guidelines.

No comments:

Post a Comment